Tax Prep vs. Tax Planning: Three Principles to Help You Keep More of What You Earn

Three-Part Series Overview

Part 1: Foundational tax-planning principles (Tax-Savvy Wealth Guide Principles 1–3)

Part 2: Income, equity, and complexity for ambitious professionals (Tax-Savvy Wealth Guide Principles 4–6)

Part 3: Retirement, legacy, and multigenerational planning (Tax-Savvy Wealth Guide Principles 7–9)

At a Glance: The Principles Covered in This Article

If you only read one section, start here.

- Tax preparation records what has already happened.

Valuable for compliance but limited in shaping outcomes. - Tax planning happens before decisions are locked in.

Income timing, investment structure, and benefit elections matter long before filing season. - Small coordination gaps create long-term tax drag.

Most overpayment happens quietly, not through obvious mistakes. - Your investment strategy and tax strategy are inseparable.

Account type, asset location, and activity timing influence lifetime taxes. - Life changes create planning windows.

Career moves, equity events, retirement timing, and family transitions all trigger tax consequences.

At Affinity Financial, these principles guide how tax planning is approached across income, investments, and life transitions—rather than in isolation.

Keeping more of what you earn isn’t about being clever during tax season. It begins with understanding the quiet but powerful difference between tax preparation and tax planning; one records the past, the other shapes the future. If you want your financial planning to support the life you’re building, not chip away at it, that distinction matters more than most people realize.

You’re earning well, saving diligently, and investing consistently. By most measures, you’re doing everything “right.” Yet for many high-income professionals and successful retirees, the real threat to long-term wealth isn’t market volatility or overspending. It’s the slow drip of avoidable taxes—dollars lost simply because no one was watching the right things at the right time. Even strong savers can lose thousands (or tens of thousands) over their lifetime without a coordinated, tax-aware plan.

That’s the difference between tax prep and tax planning.

- Tax preparation is what happens after the year is over.

- Tax planning is forward-looking and can meaningfully shape your future.

It’s an important distinction. Tax planning isn’t a single tactic or a once-a-year conversation. Instead, it’s an approach that touches every major financial decision you make. That’s the heart of what this three-part blog series explores. Each post will highlight three principles from Affinity Financial’s Tax-Savvy Wealth Guide and show how tax planning weaves into every part of your financial life.

Today, we begin with the first three principles: universal practices that apply whether you’re early in your career, leading a high-earning household, or already enjoying retirement. These often overlooked strategies can make a meaningful difference when you start applying them.

👉 1. Tax-Smart Planning Happens Before You File

Proactive coordination turns routine filing into real strategy.

Smart people overpay taxes all the time—not because they don’t have good professionals around them, but because no one is consistently connecting the financial dots throughout the year.

Most CPAs are excellent at filing what’s already happened. But true financial progress comes from what happens before the year ends. That’s why you need a tax awareness system—a forward-looking framework that aligns income timing, investment moves, and strategic elections into one cohesive plan.

The lack of a tax-aware strategy is not your fault. The gap often exists because most people assume that tax planning is automatically part of their relationship with their CPA. However, unless someone is actively coordinating your finances before December 31st, you’re likely missing out on opportunities to optimize. Tax planning shouldn’t be an afterthought; it should be built into every decision that affects your wealth. When executed properly, tax planning isn’t just compliance. It’s a proactive, high-impact wealth strategy. Each of these is a moment where a tax-aware advisor can help you keep more of what you earn:

- Multi-year income planning to optimize for total eligibility on deductions and credits

- Capital gains and loss harvesting coordination

- Adjusting withholdings or making timely estimated payments

- Strategically maximizing workplace and self-employment benefits

💡 Think of it this way:

Filing is like writing the history of last year.

Planning is proactively writing a better story for the years ahead.

Tax Prep vs. Tax Planning: Know the Difference

| 📄 Tax Preparation | 🧠 Tax Planning |

|---|---|

| Focuses on last year | Focuses on this year and beyond |

| CPA completes your tax return | Advisor + CPA collaborate before year-end |

| Done by April 15 | Happens year-round |

| Reactive: based on what already happened | Proactive: shapes what will happen |

| Often siloed | Integrated with your income, investments, and goals |

👉 2. Your Investment Plan Is Your Tax Plan

The most effective portfolios are built with the tax code in mind.

Some of your biggest tax savings (or missed opportunities) are determined by the structure of your portfolio today. Factors like type of account, type of investment, and timing of activity all affect how much tax you’ll owe—this year and over your lifetime.

When designed intentionally, your investment plan doesn’t fight the tax code—it works with it.

💡 Common Causes of Silent Tax Drag:

- Too much cash or taxable bond interest in brokerage accounts, taxed at the highest rates

- Actively managed mutual funds that surprise you with capital gain distributions—even if you didn’t sell anything

- All savings stacked in pre-tax accounts, which limits withdrawal flexibility and can spike taxes in retirement

- Missing out on tax-favored income, like qualified dividends, municipal bond interest, or U.S. Treasury income

- Stock sales or option exercises that aren’t coordinated with your broader tax plan, leading to unexpected liabilities

Withdrawal coordination is one of the clearest places where real-world tax experience pays off. A well-timed Roth withdrawal or a shift in sequence can significantly impact your assets without altering your lifestyle.

📊 Case-in-Point:

Sarah, a high-income professional, held a large portion of her portfolio in actively managed mutual funds within a taxable account. Even though the funds underperformed, she was hit with a surprise $12,000 capital gain distribution—adding tax liability without real returns.

By moving toward diversified stocks and tax-efficient ETFs in her brokerage account and shifting bond exposure to her pre-tax IRA, she maintained her strategy while reducing unnecessary tax friction.

The real win for Sarah wasn’t about chasing higher returns—it was about reclaiming control. Her portfolio started working smarter, not harder, because it finally worked with the tax code instead of against it.

✅ The Smart Move:

Review your asset location (where you hold investments), not just your allocation. Align high-growth and tax-inefficient investments inside retirement accounts. Use taxable accounts for low-turnover or tax-advantaged holdings. Additionally, consider tax-aware strategies, such as direct indexing or tax-loss harvesting, to actively manage your tax exposure over time.

Small structural shifts can add up to meaningful, long-term savings, freeing you to focus more on life and less on the IRS.

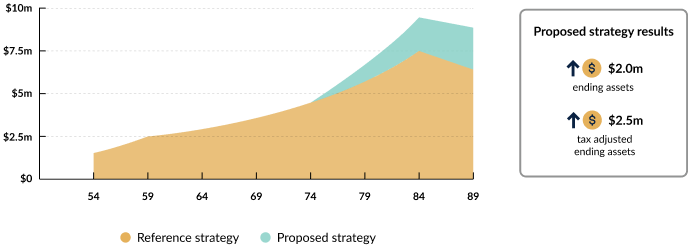

why assets location matters

*Illustrative proposed strategy. Actual results can differ.

portfolio tax drag: before vs after

*Illustrative proposed strategy. Actual results can differ.

👉 3. Your Life Transitions Should Trigger Tax Strategy Updates

Every new chapter brings a chance to realign your financial story.

Marriage, divorce, career moves, a new child, a business launch, a big equity event—these transitions all come with new tax implications. Too often, people delay adjusting their strategy until tax time, when it’s already too late to optimize. View every life change as an opportunity to recalibrate your financial plan for real savings.

💡 Smart Moves During Life Changes:

- Newly married? Coordinate benefits, align income brackets, and avoid duplicate contributions or missed deductions.

- Switching jobs? Review stock options, rollovers, and benefit elections before year-end.

- Growing family? Maximize utilization of dependent care FSA and HSA, and spousal IRA contributions.

- Business side hustle? Evaluate Solo 401(k), QBI deductions, and cash flow timing for estimated payments.

The best plans evolve with your life. The goal is to make every transition, big or small, an opportunity to strengthen, not disrupt, your foundation.

💬 Tax Insight: When Rachel and Daniel got married, they assumed “married filing jointly” was just a checkbox. However, once they examined their combined income, equity compensation schedules, and overlapping benefits, the picture changed. By staggering their equity exercises across two years and optimizing which employer offered better pre-tax perks (like HSA, FSA, and 401(k) match), they reduced their adjusted gross income enough to qualify for the full $40,000 SALT deduction and $2,200 child tax credits—saving over $14,000 in that year alone.

🔁 Planning Prompt: What’s changed in your life over the past 12–18 months? Have you revisited your household financial and tax strategy to match? Whether you file Single or share income and benefits with a spouse, transitions like marriage, divorce, career changes, or having kids can create tax-saving windows—or tax traps. Coordination matters more than ever.

Your Tax Awareness Starts with One Simple Step

Tax planning becomes easier the moment you know where your current approach is strong—and where more coordinated planning may add value. Affinity Financial’s Tax Awareness Self-Reflection Survey draws on our years of real tax experience to help you view your choices through a more strategic lens. It’s a simple way to see how your day-to-day financial decisions align with long-term tax strategy.

Take the survey to see where your strategy stands today.

Are you overpaying taxes?

Take the 2-minute quiz to find out.

EXPLORE TOPICS

Start Your Next Chapter and Pursue Exciting Financial Goals

Click below and schedule a complimentary consultation

Similar Posts

No results found.