The Role of Cash Savings: A Buffer for Long-Term Resilience

The $2,500 That Changed Stephen King’s Life

In the early 1970s, Stephen King was living in a trailer, working as an English teacher and barely scraping by. He wrote stories in his spare time, but rejection after rejection piled up. Frustrated and financially struggling, King threw a draft manuscript into the trash, convinced it wasn’t worth pursuing.

His wife, Tabitha, retrieved it and urged him to keep going. King finished the story and sent it off once more. Soon after, the publisher Doubleday accepted his novel, offering the author a modest but critical advance of $2,500. That wasn’t a lot of money, yet the injection of cash served as a crucial lifeline. The financial cushion gave King breathing room, allowing him to support his family and continue writing with less pressure.

That discarded manuscript was Carrie, King’s first novel, which became a bestseller and launched one of the most remarkable literary careers of all time.

That buffer—cash in hand—wasn’t just about money. It was about emotional resilience, freedom from immediate pressure, and the opportunity to continue chasing dreams. King’s modest cash cushion protected him from life’s volatility and allowed him to seize an opportunity he nearly lost.

The Role of Cash: Why We Hold It

Cash is foundational in money management—not just for survival, but for fueling growth.

We hold cash as permission to keep playing the game—the game of investing, the game of wealth-building, the game of life.

Cash is a buffer, a shock absorber, a safety net stretched between where we are and where we want to go. Long-term wealth is built by those that manage the short-term well enough to stay in the game for the big rewards to come.

The right amount of cash turns a financial crisis into an inconvenience. Holding the wrong amount? That’s when real damage happens.

The Benefits and Risks of Holding Cash

We hold cash because life—and markets—humbly remind us that things are uncertain.

Cash-on-hand provides some key benefits:

- Liquidity: Available immediately, without selling assets or taking on debt.

- Emergency Reserves: A cushion for the unexpected. Things like job loss, medical bills, or car repairs.

- Opportunity & Flexibility: When markets wobble or life presents an opportunity, cash lets you act.

- Risk Mitigation: A buffer against market volatility so you’re not forced to sell at the worst time.

- Psychological Comfort: Knowing you can handle unexpected expenses without panic or stress.

- Current Income: Cash can earn interest, boosting short-term returns.

But it is essential to recognize that cash also has its downsides:

- Low Long-Term Returns: Cash typically underperforms compared to stocks, real estate, or bonds.

- Opportunity Cost: Too much cash means missing out on long-term compounding growth.

- Inflation Erosion: Over time, inflation eats away purchasing power.

- Tax Drag: Interest income is taxed at the highest rates, eating into returns.

Now that we understand the role of cash, let’s explore how to determine the right amount for you.

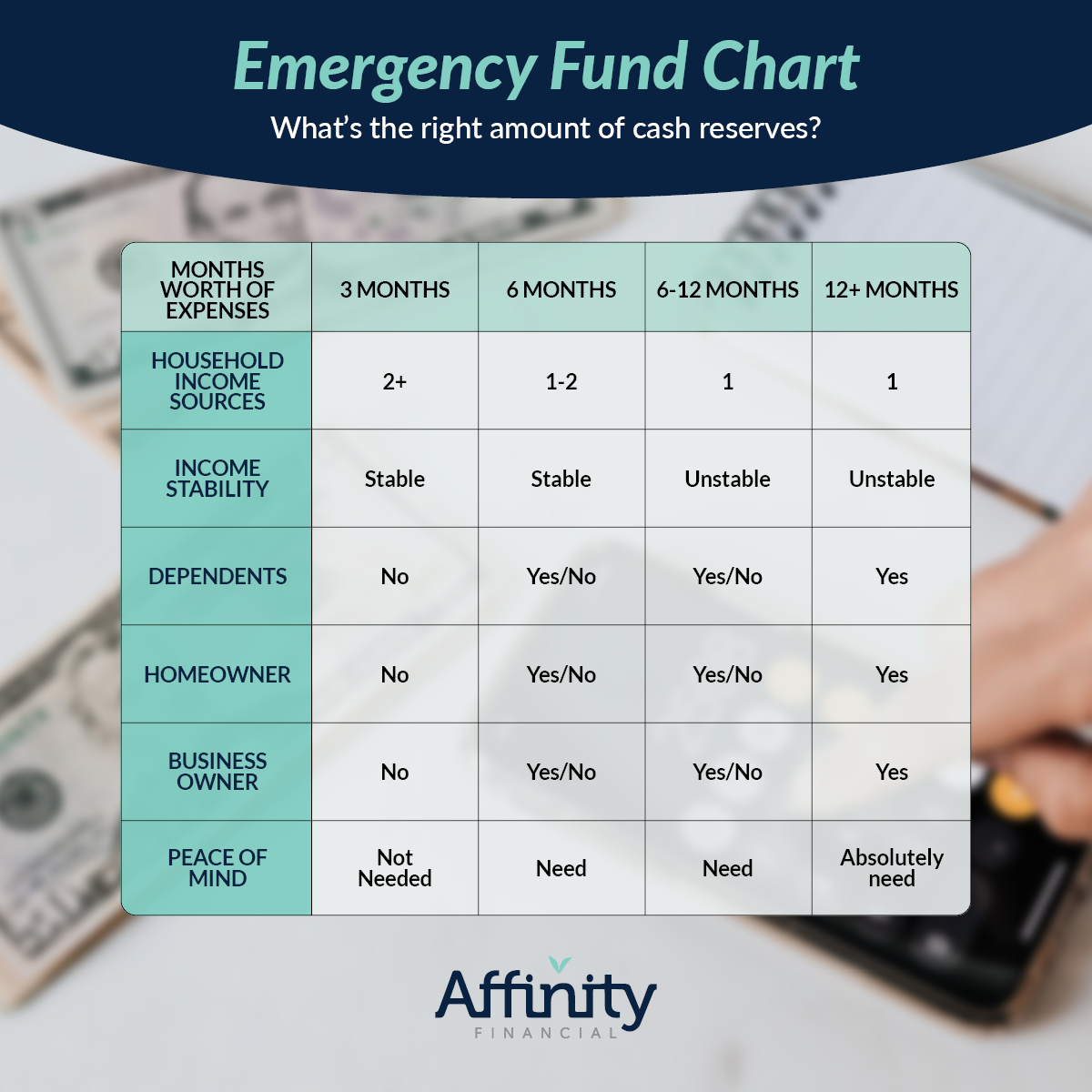

How Much Cash is Enough?

The “right” amount depends on your individual circumstances. Consider your stage of life, household income sources, personal and professional responsibilities, and psychological comfort. Think about about cash holdings in terms of months of spending. Ultimately, this buffer is buying time—time to think clearly, time to act accordingly, and time to return focus on your bigger picture life objectives.

Major factors in determining your ideal cash targets may include:

Here’s a useful framework for how much and where to hold your cash:

Bank Checking – The Operating Account

- Purpose: Cover your monthly expenses.

- Benefits: Easy access, bill-paying simplicity, everyday transactions.

- Typical Cash Target: 1.5- to 3-months of typical monthly expenses. You need to know your typical monthly spending amount, but the reality is that expenses will fluctuate throughout the year. Holding a cash buffer in a checking account allows for the natural ebb and flow of cash while avoiding unnecessary overdrafts and stress.

High-Yield Savings – The Emergency Reserves

- Purpose: Preparation for unexpected life events.

- Benefit: Retains need for stability, liquidity, and earns interest.

- Typical Cash Target: 3- to 6-months of spending is a good place to start. Add more if you’re self-employed, in a volatile industry, have irregular income, or crave extra peace of mind. For business owners, retirees, and those with highly unpredictable income, the cash target may need to be increased further toward 6- to 12 months or more.

High Yield Savings, Treasury Bills, Money Market Funds, and/or CDs – Planned Large Near-Term Expenses

- Purpose: Pre-fund significant life expenditures that go beyond regular spending.

- Benefit: Focus on stability, liquidity, and interest earnings. While more aggressive investments could potentially yield higher returns, the primary goal for these near-term objectives is to ensure they happen without taking unnecessary risks or setbacks.

- Typical Cash Target: Determine the exact amount needed for major life goals in the next 12-18 months that go beyond typical household spending—such as a home down payment, car purchase, family vacation, or wedding. This amount should cover your anticipated expenses without risking it in volatile markets.

Common Cash Mistakes (and How to Avoid Them)

Many people make the same mistakes when it comes to managing cash. Here’s how to avoid them:

- Holding too much cash: Fear or lack of strategy can cost you years of potential compounding returns. Set a clear cash target based on needs and invest anything beyond that.

- Holding too little cash: Overconfidence or wishful thinking can lead to bad outcomes when an unexpected events strike. Take an honest assessment of your emotional risk tolerance and financial risk capacity.

- Using emergency funds for lifestyle spending: Emergencies are unpredictable. Vacations, property taxes, gadgets, and gifts are not emergencies. Incorporate likely, but infrequent expenses into your annual spending plan.

- Mixing checking and savings: Keep clear boundaries between operating expenses, emergency funds, and near-term savings needs.

- Not earning high-yield interest on savings: Your cash should work for you, not your bank. Utilize a high-yield savings account or low-risk cash alternatives to earn more than idle cash in a non- or low-yielding bank account.

- Too many accounts: Keep your cash organized and strive for simplicity. Each account should serve a clear role and purpose.

- Not automating savings: Don’t rely on good intentions. Set up a system that delivers your desired outcomes by automating transfers into savings and investments.

How This May Play Out in Real Life

- A young professional: Needs 3–6 months of expenses in high-yield savings but should aggressively invest anything beyond that.

- A business owner with variable income: Needs a larger cash reserve—potentially 9–12 months—to manage unpredictable revenue.

- A retiree drawing income from investments: Needs a mix of cash and other income-producing assets to fund multiple years of spending, allowing them to remain invested in stocks for long-term retirement objectives, especially during market fluctuations.

Find Your Cash Sweet Spot for Stability and Opportunity

When Stephen King received his first small advance for Carrie, it wasn’t life-changing money—yet. But it was enough. Enough to give him breathing room. Enough to allow him to keep writing. Enough to ensure he didn’t have to give up on what would become one of the most successful literary careers of all time.

That’s exactly what cash is supposed to do in your personal finances.

Cash isn’t about maximizing returns. It’s about minimizing risk.

Warren Buffet famously said that cash is the financial equivalent of oxygen—unnoticed when it’s there, but critical when it’s not.

The right cash strategy helps ensure you don’t get knocked out of the game.

Holding enough cash doesn’t make you rich. But running out of cash can make you poor.

With the right amount of cash:

- A job loss is stressful, but it’s not disastrous.

- A medical bill is inconvenient, but it doesn’t derail your long-term goals.

- A market downturn is an opportunity, not a reason to panic.

But too much cash? That’s a different problem. Holding excessive cash beyond your needs is like hoarding oxygen tanks while sitting in fresh air—eventually, it becomes wasted potential.

The balance is found with enough cash to weather storms without being forced into bad financial decisions, but not so much that you sacrifice long-term compounding growth and let inflation erode your purchasing power.

A Framework for Smart Cash Management

- Establish Cash Targets: Define how much cash you need based on income stability, risk tolerance, and near-term goals.

- Segment Your Cash: Separate between daily spending, emergency reserves, planned large expenses.

- Earn Competitive Cash Returns: Use high-yield bank savings low low-risk holdings, like Treasury Bills or money market funds.

- Automate Your System: Ensure cash flows effortlessly to the right places.

- Review and Adjust: Regularly revisit your strategy as life changes or your financial situation evolves.

The right amount of cash doesn’t make you rich overnight, but it prevents chaos that can keep you from getting there.

This isn’t about a perfect number. But it is about an optimal system—one that keeps you protected while allowing you to grow.

Not too much. Not too little. Just enough to transform uncertainty into confidence, chaos into resilience, and crisis into nothing more than a bump on the road to long-term success.

Manage your cash holdings thoughtfully, so that a temporary life or market event is a nuisance—but not a catastrophe. Hold enough cash to keep moving forward—no matter what life throws at you.

Are you overpaying taxes?

Take the 2-minute quiz to find out.

EXPLORE TOPICS

Start Your Next Chapter and Pursue Exciting Financial Goals

Click below and schedule a complimentary consultation

Similar Posts

No results found.