Keeping a Mindful Eye on Inflation

If you are not confused about the global economy, you don’t understand it.

Charlie Munger

I continue to believe that the American people have a love-hate relationship with inflation. They hate inflation but love everything that causes it.

William E. Simon

In our recent “Summer Economic Update – A Quick Temperature Check,” we discussed the economy’s recovery and expansion over the past year. If you haven’t read this yet, we encourage you to do so.

In this article, we address one of the key economic risks that is commonly being discussed: inflation.

What Exactly Is Inflation?

To begin our conversation on inflation, we need to start with a common understanding. Defined simply,

inflation refers to the gradual rise in prices over time, meaning the dollars you have today won’t stretch as far tomorrow. Inflation is experienced as a decline of the purchasing power of a given currency over time.

Inflation, though, isn’t necessarily a bad thing. Economists use the broad increase (or decrease) in prices of goods and services across the country as a measure of economic health. When inflation is stable and predictable, it’s a sign of a basically healthy, growing economy.

What Is A Healthy Level Of Inflation?

Since 1977, the Federal Reserve has been tasked with fulfilling two mandates. The first is inflation stability, and the second is maximum sustainable employment. Currently, the Fed aims to maintain an average inflation rate of 2% over time.

Why 2%? In truth, it’s a bit arbitrary. This ‘reasonable level’ is essentially determined by what people have come to expect. If you are interested in learning more, the Federal Reserve has a dedicated page called “Why does the Federal Reserve aim for inflation of 2% over the longer run?” on their website.

Theoretically, when consumers can reasonably expect an average inflation rate of 2% over the long run, they’re incentivized to spend and invest their money today, while their dollars are worth more. This, in turn, contributes to a well-functioning economy.

There is a bit of the ‘Goldilocks principle’ at play here. We don’t want it “too hot,” nor “too cold.”

Too high of an inflation rate can quickly eat away at the purchasing power of your dollars, indicating that the economy might be overheated. This often happens because when there’s more demand than supply, prices will go up. This can also happen when an external event, like a natural disaster or a pandemic, makes it harder for companies to produce enough to keep up with consumer demand and they raise their prices.

Deflation, or a decline in prices, however, can be a warning sign of a shrinking economy.

Why Can Inflation Feel So Threatening?

Inflation can feel threatening because when it is not ‘reasonable,’ it can quickly erode hard-earned purchasing power and undermine consumer confidence.

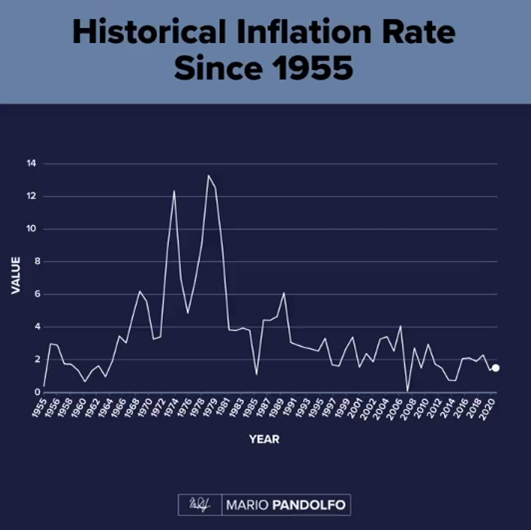

In the 1970s, President Gerald Ford declared inflation “Public Enemy Number One.” President Jimmy Carter called it the nation’s “most serious domestic problem.” This was a time when the country was gripped by double-digit inflation that required painful action by the Federal Reserve.

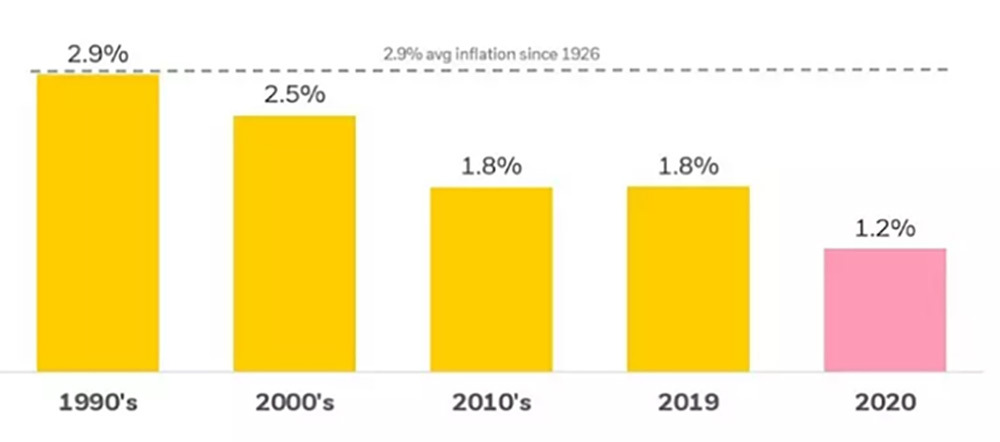

During the 1970s, annualized core inflation averaged 6.8%; an inflation rate that indicated prices would double every 10.3 years. In contrast, the 2010s delivered an annualized core inflation of 1.9%, translating to a doubling of prices every 37.1 years.

Why Are People Concerned About Inflation Now?

No one disputes that inflation has arrived. The number of companies citing inflation in their earnings calls has hit a 10-year high.

The question is, where is inflation heading?

Extraordinary fiscal and monetary policies from the government over the past 18 months have stoked investors’ inflation expectations, as there has been an incredible $4.2 trillion increase in the money supply over the past year. This means that there are substantially more dollars in existence now than prior to the pandemic.

Buoyed by transitory factors tied to supply chain bottlenecks and low comparisons to a year ago, it was a foregone conclusion that inflationary metrics would appear as global economies opened back up in 2021.

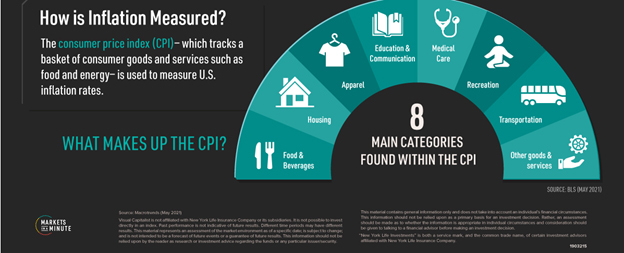

The Consumer Price Index (CPI) is the most common proxy of inflation for the average American consumer. This index acts as a representative basket of products and services that are routinely purchased. For June, the Bureau of Labor Statistic’s headline CPI figure stood at 5.4% year-over-year, the second-highest rate in 30 years. When excluding food and fuel, which tend to have higher monthly variability, core CPI inflation still comes in at 4.5% — its highest in three decades, by far. Even if the most extreme price movement outliers, both up and down are stripped out, inflation stands at 2.9%, a near worst since 1992.

It’s useful to know that most measures of inflation compare what’s happening now with what was happening a year ago. This time last year, the U.S. economy shut down because of COVID-19. In April 2020, oil prices collapsed and this was passed on to consumers in April and May. The yearly change in inflation rate in the second quarter (months April to June) of 2021 will, therefore, be compared to an abnormally low oil price. This so-termed ‘base effect’ is likely to end only in the second half of the year. Investors, therefore, must be aware that the economic impact of the pandemic is going to distort any year-over-year comparisons for a while longer. A short-term spike following a very weird period for the economy is not causing alarm yet; we should prepare ourselves for more odd numbers coming out of different parts of the economy in the weeks and months to come.

Is This Runaway Inflation or The Normalization of Prices As The World Reopens?

Inflation concerns are legitimate, but widespread alarm may be slightly overdone.

While the dual demand shocks of the fiscal stimulus package direct payments and post-pandemic reopening have created acute price pressures in a concentrated handful of industries, inflation for most goods and services is up only modestly over the past year.

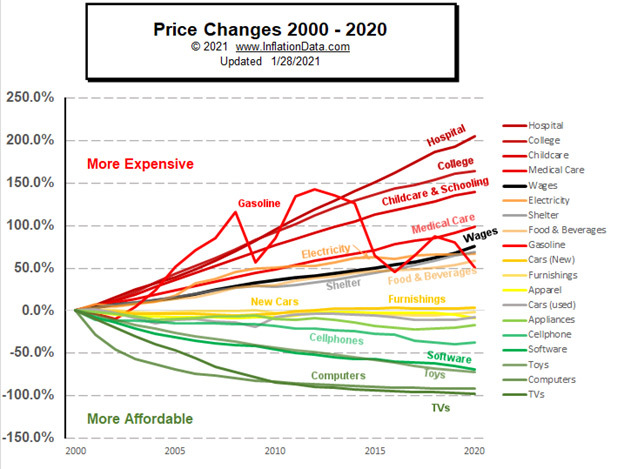

As households are well aware, not all inflation is created equal:

- If you are saving for a child’s college education, you are focused on college education inflation.

- If you drive a lot and need to constantly fill up your tank, you are dialed into the cost of gas.

- If you are looking to make a home purchase, you will be tracking housing prices.

While the Consumer Price Index (CPI) attempts to capture the inflation for the average consumer, this isn’t necessarily reflective of your own personal inflation rate. Everyone’s basket of goods and services looks different. So, when the media reports a jump in CPI, don’t assume your expenses are increasing at the same rate.

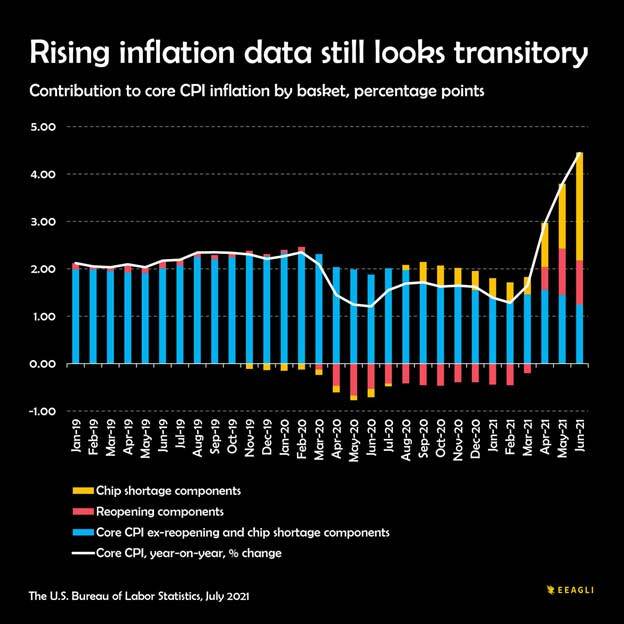

Moving forward, it is sensible to assume that automobile chip shortage and many other supply-chain difficulties related to the global economic re-opening are temporary in nature. Same for the leisure and hospitality prices fell the most during the pandemic. This should resolve much of the more immediate inflationary pressures.

For categories like housing prices and wages, we might reasonably expect inflation to slow down, but for higher prices to remain. Likewise, inflation caused by industrial metals, fuels, and agricultural commodities may linger a bit longer. These are categories where demand outweighs supply, and it may take some time for the two to find balance.

Still, there are likely goods and services in which we have yet to see material price increases, such as home rents or small business services that feel pressured by higher wages. It is possible that a period of persistent inflation, driven by higher wages and feeding into higher prices, could lead to tighter financial conditions and put this young economic expansion in jeopardy. Nevertheless, we remain in the camp that expects inflation to moderate from here, for several key reasons based on structural trends.

Key Long-Term Structural Forces: Employment, Demgraphics, Technology, and De-Globalization

In our current environment, the ongoing wage tracker kept by the Atlanta Fed shows that wage inflation for low-skilled workers has reached 3.6%, close to its highest since the global financial crisis.

As virus-related obstacles diminish, it is likely that the U.S. labor supply will increase and ease upward wage pressures.

Historically, inflation tends to emerge as the labor market tightens and businesses must pay more for workers. This generally occurs as the natural rate of unemployment falls between 3.5% and 4.5%. With the US unemployment rate at 5.4% as of July 2021, there is still plenty of time before the economy achieves full employment since labor markets tend to not move as fast in recoveries as they do during downturns. Notably, however, this relationship did not hold in the latter part of the 2010s when sub-4% unemployment levels did not lead to an acceleration of inflation.

Demographic trends are also likely to be a persistent headwind to inflation. The combination of falling US population growth and the increase in the average age of the population actually suggests lower inflation trends.

Technology and innovation are major forces that have kept inflation at lower-than-average levels since the 1990s. In fact, goods like computers, software, phones, and televisions have all decreased substantially in price during this period while also improving dramatically in quality. Over the last year, companies across every sector of the economy invested in productivity-enhancing technology. According to The Wall Street Journal’s report Business investment in consumer equipment and software rose by 17% and 6%, respectively, in the fourth quarter of 2020 alone. Companies also invested more in automation, videoconferencing software, and enterprise cloud services. Investing in technology puts downward pressure on input prices and in many cases, increases productivity per worker – two deflationary forces.

There is a trend that may prove to be inflationary in the long-term: de-globalization. This is a reversal of the globalization that has lowered prices over the past few decades. Even before the pandemic, the US set plans into motion to bring manufacturing back to the US as a measure of national security and to develop a more robust supply-chain infrastructure. This will likely bring jobs and a lot of automation, but also higher wages and thus higher costs. This policy will also be coupled with moving additional manufacturing capacity toward low-cost countries that are considered friendly to the US, such as India and Mexico.

Keeping an Eye on Inflation

While higher inflation beyond 2021 is certainly a possibility and something to keep an eye on, it is not a foregone conclusion. Ultimately, there are several significant factors combating the potential for persistent and meaningful long-term inflation.

It does appear that we will see some stronger prices accompanying a strong economic expansion throughout the year, but we aren’t expecting a return to 1970s-style inflation. Economists surveyed in July by The Wall Street Journal, on average, expect inflation to be up 3.2% in the fourth quarter of 2021. They forecast the annual rise to recede to slightly less than 2.3% a year in 2022 and 2023. Moving forward, as the economic reopening broadens, raw materials and component shortages begin to disappear, and supplier delivery times shorten, inflation is anticipated to settle inside most central banks’ comfort zones.

From a financial planning perspective, there may be some purchases in which waiting for highly volatile prices to stabilize makes sense. For most, though, it is likely best to avoid making knee-jerk reactions.

If inflation is going to stick around for a while, it may be appropriate to make some prudent adjustments, like considering higher future inflation estimates in your long-term income planning. But this all depends on individual factors, like specific goal time horizons and the investment portfolio composition.

This is definitely not a one-size-fits-all scenario and this is why it helps to get personalized advice from a financial professional.

Feel free to reach out if you want to talk about how we’re accounting for potential inflation in your financial plan or just looking to learn more.

Disclosure: Derek Pantele is an Investment Advisor Representative with Dynamic Wealth Advisors. All investment advisory services are offered through Dynamic Wealth Advisors. All investments carry certain risks and there is no assurance that an investment will provide positive performance over any period of time. Past performance is not a guarantee or a reliable indicator of future results. The views expressed within are subject to change at any time without notice and are not intended to provide specific advice or recommendations for any individual or on any specific security or strategy..

Are you overpaying taxes?

Take the 2-minute quiz to find out.

EXPLORE TOPICS

Start Your Next Chapter and Pursue Exciting Financial Goals

Click below and schedule a complimentary consultation

Similar Posts

No results found.