Summer 2021 Economic Update – A Quick Temperature Check

From a market perspective, the first half of the year has been about significant economic recovery and expansion in the wake of a global pandemic.

This continuation of global economic growth remains the most dominant theme in determining the direction of the stock market.

The simple truth is that economic fundamentals, such as corporate earnings, small business growth, investment, the consumer, and innovation remain the most important metrics to track. By dialing in on the potential growth catalysts and risks at the macroeconomic, business sector, and company levels, we can be best prepared to focus our attention on the real issues that impact your investment portfolio. This is what helps us sort “the news” from “the noise.”

For these reasons, we are going to highlight some noteworthy Summer 2021 economic factors and trends.

Economic Recovery & Expansion

Moving Past Peak Pandemic with Public Health Measures and Scientific Innovation

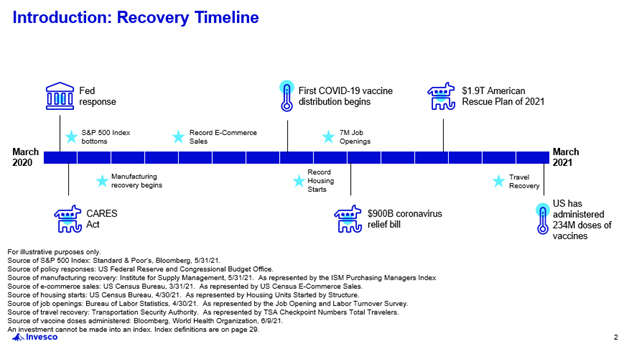

The COVID pandemic has been a rollercoaster that nobody signed up for, but everybody has experienced in some way.

According to the U.S. Business Cycle Dating Committee of the National Bureau of Economic Research, the US pandemic-related recession only lasted two months, with a low point reached in April 2020. While the country had by no means get back to normal operating capacity after two months, indicators of both jobs and production “point clearly to April 2020 as the month of the trough,” with a rebound beginning in May.

Similarly, the S&P 500 hit a low on March 23, 2020, and has trended positive since generally looking through the end of the pandemic.

The pending conclusion of this widescale public health event has continually been linked to economic recovery and expansion.

While the story is still being written, it largely appears that public health data over the past few months have indicated that the global pandemic, measured by a number of cases, likely peaked in the second quarter of 2021. Despite a bumpy start, vaccination rates across developed markets have accelerated. As a result, global rates of hospitalizations and deaths are likely to continue to decline overall, despite the slower vaccination rates in emerging markets countries.

Though the true impact of variants is still largely unknown, and some regions are experiencing varying rates of vaccine hesitancy, it appears that scientific technologies and societal adaptations have likely permitted the US and other developed markets to get through the worst of the global pandemic.

Public Policy Leadership Transitions into Consumer & Business Leadership

Whether you totally agree or disagree with the monetary policy measures by the Federal Reserve and the fiscal policy from Congress over the past 18 months, it is generally accepted that quick and aggressive actions to maintain economic and financial system core stability were largely necessary.

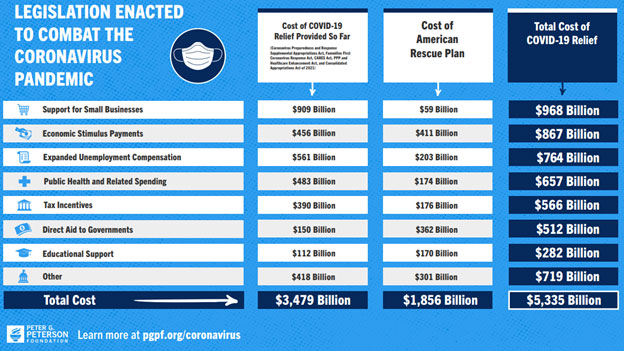

In total, US lawmakers enacted six major bills, costing about $5.3 trillion, to help manage the pandemic and mitigate the economic burden on families and businesses.

With the pandemic receding, policy support is likely to have also peaked.

Stimulus checks and other funding from the American Rescue Plan have mostly ended and pandemic-related unemployment assistance will end by early September (with half the states cutting benefits sooner than that). Infrastructure and other spending proposals have been pushed back in time and size.

While the merits of future economic policy will be debated, the Federal Reserve has vowed to remain largely supportive of continued economic growth measures for the time being, and there are positive indications that consumers and companies can once again lead our economy forward.

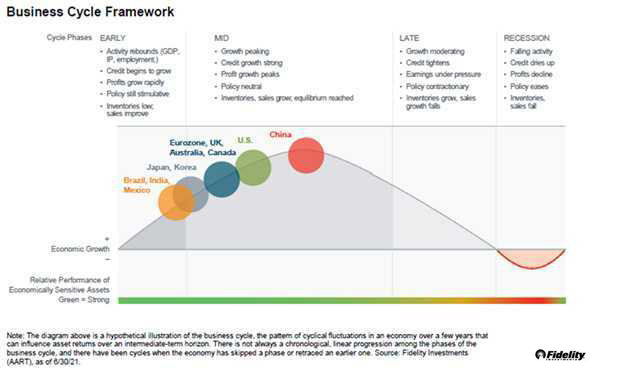

Peak Growth: From Recession to Recovery to Expansion

A business cycle, sometimes called an “economic cycle,” refers to a series of stages in the economy as it expands and contracts. Understanding the different phases of a business cycle can help: individuals make lifestyle decisions, investors make financial decisions, and governments make appropriate policy decisions. Generally, a full business cycle lasts 7 to 10 years, but this can vary.

The second half of 2020 represented the early stages of the business cycle with economic recovery stimulated through monetary and fiscal policy.

The first half of 2021, with rapidly increasing vaccination rates and a more fully re-opening economy, has brought us beyond the recovery phase and into the expansion phase. According to Fidelity Investments, the global economy is now in the early-to-middle stages of the business cycle. This mid-cycle characterization means that growth has been above average and is accelerating.

According to Pimco’s June outlook, the U.S., United Kingdom, Canada, and China likely achieved peak growth for 2021 in the second quarter, while the European Union and Japan will likely peak in the third and fourth quarters, respectively.

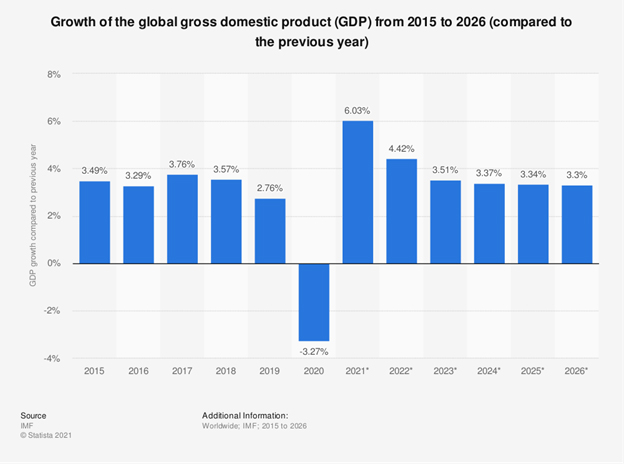

Global Growth Expectations Have Continued To Impress This Year!

A recent report by Morgan Stanley economists outlined why they think this recovery has staying power, with forecasts for 6.5% global GDP growth for 2021—led by the U.S. economy’s 7.1% growth. Currently, for 2022, it is forecasted there will be 4.8% global GDP growth, with 4.9% growth for the U.S. For reference, global GDP growth had averaged 3.4% in the five years preceding the pandemic, with the US growth averaging 2.5% during that time frame.

Record Savings

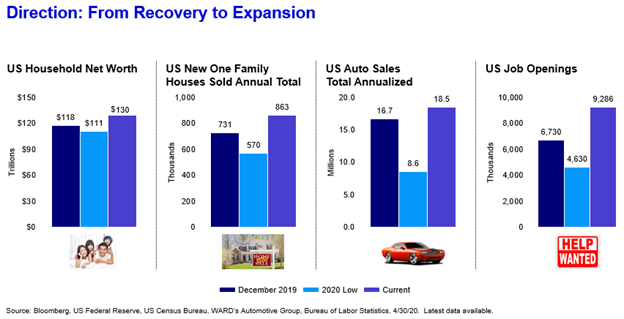

As you can see, the growth expectations are quite staggering, but they make sense if you look at the resilience and strength of the consumer. Despite higher levels of unemployment over the past year, average U.S. household income—bolstered by economic-impact payments and supplemental unemployment benefits—has already exceeded its pre-COVID level. In addition, many households have excess savings due to the pandemic. Americans were able to save money in record amounts during the downturn, thanks to government stimulus payments combined with business closures that essentially forced savings. For example, personal savings rates soared to 21% of disposable income in the first quarter of 2021 as per Capital Group’s report. U.S. households were saving at an annualized rate of $2.8 trillion in April 2021, which is two times higher than the savings rate before the crisis. According to Wall Street Journal’s report, the annualized savings rate was $734 billion in June 2009 (following the Great Recession). Accumulated savings today amount to a wall of consumer liquidity poised to power the expansion. “COVID-related spending limitations on service-sensitive parts of the economy have resulted in an impressive accumulation of savings, which can be deployed to fund pent-up demand,” says Chief U.S. Economist, Ellen Zentner.

Beyond savings, balance sheets for households and businesses are also historically strong. Stock and home values are currently at or near all-time highs. According to Bloomberg’s findings, the delinquent share of outstanding debt for households fell to 3.1% in Q1 2021, which is the lowest rate since records began in 1999.

As we have all witnessed over the past few months, many households are planning to use some of their cash to take long-delayed holidays or simply get out of the house and go to dinner. Of course, while the aggregate data is encouraging, individual stories and financial circumstances vary greatly.

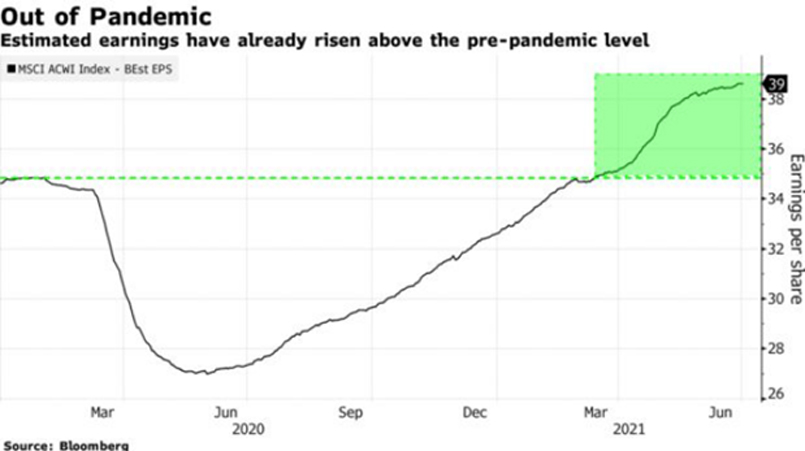

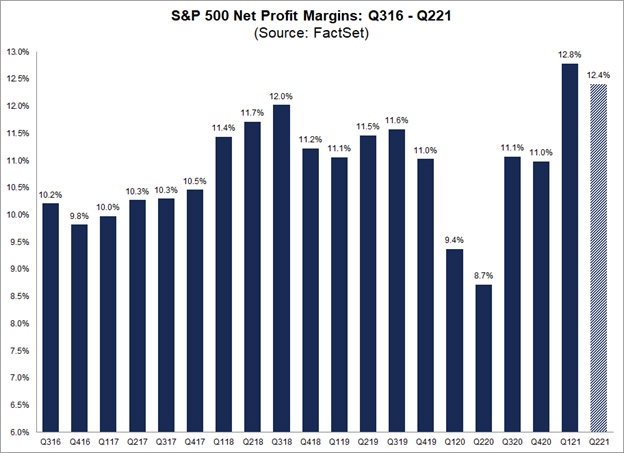

Meanwhile, S&P 500 companies are currently reporting that they are on track for the second-highest net profit margins since 2008 for the second quarter of 2021. If the anticipated profit margin rate of 12.4% is achieved, it would be above the five-year average of 10.8%, and only bested by the prior quarter’s rate of 12.8%. Furthermore, companies are still issuing record-level earnings and revenue guidance for future quarters, showing positive expectations moving forward.

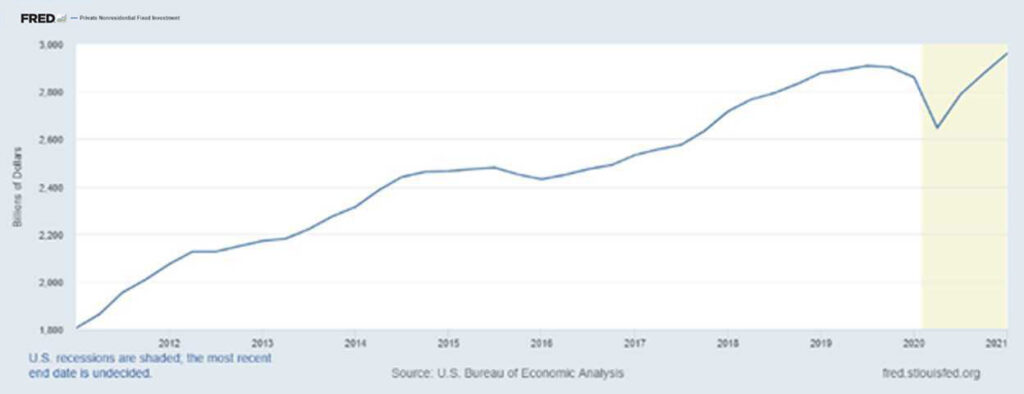

While it is widely reported that some employers are experiencing cost pressures through wage increases and supply chain shortages, this appears to be concentrated in specific sectors in which supply is falling short of demand. These imbalances should work themselves out as stimulus-induced demand and COVID-restricted supply find a new equilibrium. Overall, the margin expansion numbers show a combination of increased productivity and demand. One key area of underappreciated strength is business investment, which has eclipsed pre-pandemic highs. We’ve seen a trend in the U.S. where companies are increasing orders for machinery, software, and other equipment to expand productivity and to reshape their businesses in the wake of the pandemic.

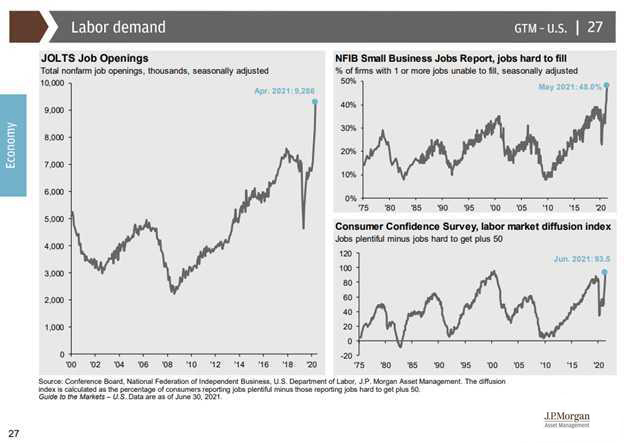

Many Jobs, Many Workers- Frictions Remain

The US labor market is also showing signs of improvement. The economy added 850,000 jobs in June, marking the biggest monthly gain in almost a year and topping expectations. Roughly 40% of those jobs came from the leisure and hospitality sectors and average hourly pay rose 3.6% year-over-year. Challenges remain, of course, as the unemployment rate now sits at 5.9%. The economy is still 6.8 million jobs short of its pre-pandemic levels—not because employers aren’t hiring, but because they’re struggling to find qualified workers willing to fill all their open positions. In fact, there is one job available for every person who is unemployed—a record 9.3 million job openings in the United States. Several factors are behind the development, including many workers moving locations, changing job preferences, prioritizing other household responsibilities, and assessing workplace safety concerns. It’s reasonable that these frictions take some time to work themselves out, especially as workers evaluate career prospects in this evolving economy. In the long run, this slow matching process could have benefits, leaving workers in jobs they prefer and making the economy more efficient.

Closing Thoughts

All-in-all, the economic picture has shown tremendous progress over the past year, graduating from recession, to recovery, to expansion. While not all countries are at equal stages of recovery or expansion, this trend is encouraging at a global level.

We felt it was important to start with a reflection of where the economy has been, and an understanding of where it appears to be heading. Often, traditional news sources like to focus more on the one-sided nature of threats and negativity. It’s simply better for their ratings and clicks—but isn’t particularly helpful for your long-term investment results.

There are risks that need to be monitored, to be sure. There are investment opportunities that likely provide better risk/reward prospects. For these considerations, active management can be layered into investment decisions for the purpose of adapting to current markets, capitalizing on emerging opportunities, or reducing overall risk with low correlation and diversifying investments.

We hope that you and your family are staying safe, staying cool, and enjoying the summer months! Personally, I can tell you that I am appreciative of the opportunities to gather with friends and family.

Do reach out if you have any questions or comments. We would love the opportunity to provide insights and continue the dialogue.

Disclosure: Derek Pantele is an Investment Advisor Representative with Dynamic Wealth Advisors. All investment advisory services are offered through Dynamic Wealth Advisors. All investments carry certain risks and there is no assurance that an investment will provide positive performance over any period of time. Past performance is not a guarantee or a reliable indicator of future results. The views expressed within are subject to change at any time without notice and are not intended to provide specific advice or recommendations for any individual or on any specific security or strategy..

Are you overpaying taxes?

Take the 2-minute quiz to find out.

EXPLORE TOPICS

Start Your Next Chapter and Pursue Exciting Financial Goals

Click below and schedule a complimentary consultation

Similar Posts

No results found.