The Prepared Investor’s Election Season Playbook

This is not political commentary. This is a showcase of how I, as an investment professional, think about the influence of election politics on investing.

Every four years in America the nation votes on our presidential leadership. These events are built up as high stakes events, with topics ranging from health care, education, geopolitics, the judicial system, the environment, taxation, the economy, and more. Of course, the topics are interrelated, and the prioritization of policies can have an impact on the general direction of our country. But (and this is a big but) we live in a democratic republic with numerous checks-and-balances. This means that progress is generally slow, which permits investors to stay ahead of the trends and invest accordingly.

I have found that while politics do impact the investing markets, individuals often overestimate this impact.

This is likely due to the fact that political issues are often inherently emotional and a reflection of our own identities. Such heightened emotions can often lead our brains to go into “fight, flight, or freeze” mode, immediately pulling focus from all other events. Both the immediacy of these issues and the accompanying peak emotional state(s) cause for the event to be stored as significant in our memories.

I believe that it is the role of a financial advisor to articulate why and how events in Washington, D.C., such as tax legislation, regulatory changes, monetary policy, and more, either do or don’t influence the investing strategy. More importantly, this must be done with a clear and impartial view of the investment landscape.

My aim in this commentary is to:

(1) Review historical presidential election data for guidance on how these events have impacted stock markets in the past

(2) Take a snapshot of some current election topics with potential market impact, and

(3) Propose how you can align your investment portfolio to maintain progress toward your most meaningful financial objectives.

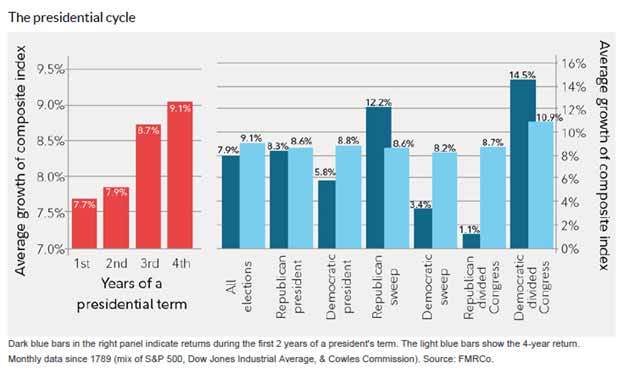

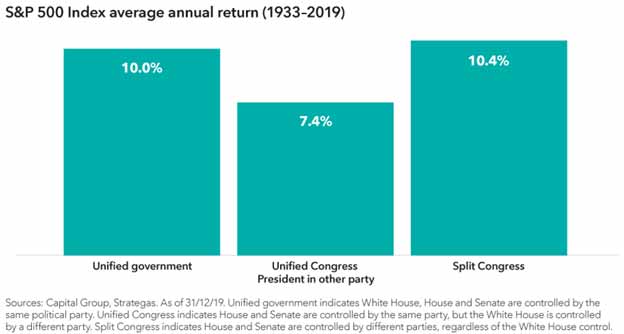

Historically, Strong Stock Market Returns Have Persisted Under Various Election Scenarios

Voters may have a strong preference for their candidates and political outcomes, but investors should take comfort that various presidential and congressional majority scenarios have historically produced strong equity returns.

Some have called the 2020 election the most important election of our lifetime. Maybe it is, or maybe it isn’t. If we honestly search our memories, though, we may agree that this tends to be said about all elections. I would bet that it will be said again about future elections as well.

Past election campaign cycles have included plenty of controversy and uncertainty. Nevertheless, in each case the market continued to be resilient. By maintaining a long-term focus, investors can position themselves for a brighter future regardless of the outcome on election day.

What About Delayed Election Results?

Due to the pandemic, a record amount of mail-in voting is anticipated. This, in addition to tight races in swing states, means that it may take a while to process the results. At this point, it is generally expected that we may not have clear results the day following the election.

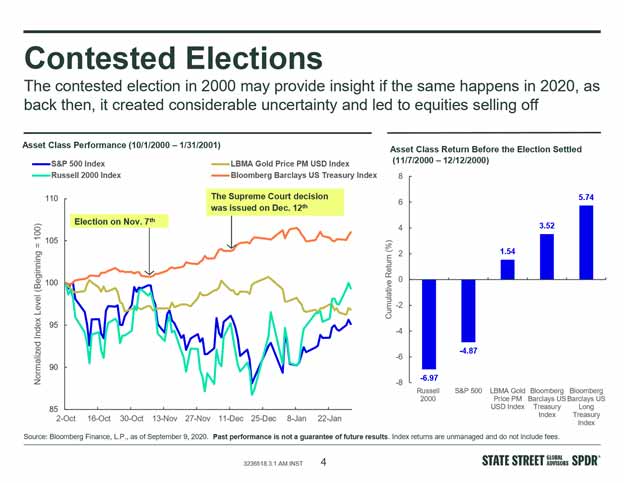

In recent years, the 2000 election between George W. Bush and Al Gore points toward an example of delayed results. The S&P 500 was down 4.8% between the November 7th election and the victor declaration on December 13th. However, it is difficult to use this one-time event as a clear parallel, as the slide in the stock index came amidst the dotcom bubble, when equities were trading excessively expensive compared to bonds. Furthermore, the contested election was a surprise.

If any lesson is to be learned from the 2000 election, it is that a diversified portfolio—inclusive of bonds and gold—can dampen total portfolio volatility. The key is to make sure that your portfolio is aligned with your total return and risk profile.

Nobody can be sure how quickly the election votes will be tallied, but I remain confident that fair election procedures will be followed and that election results will be provided when available. Speculation to the contrary is not in line with a profitable investment strategy.

Are Today’s Nervous Investors Fueling Future Returns?

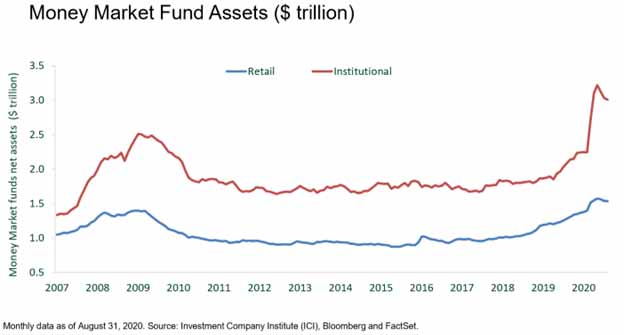

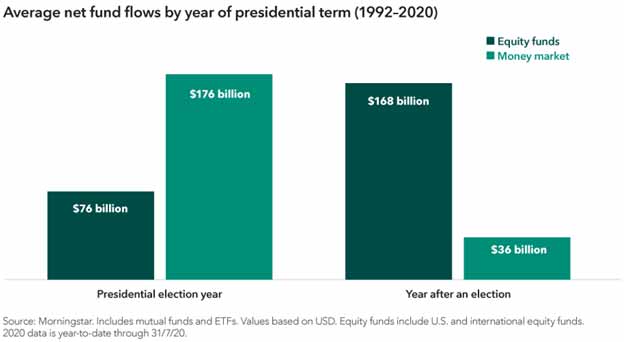

It is not shocking that investors get more nervous and increase cash positions in election years. Presidential campaigns often repeatedly mention and address the many problems the nation is facing (and how they are best suited to fix it). No wonder it seems like the stakes are so high. With so much attention on the negative, worries can overwhelm the mind, leading to increased conservatism with investing.

It appears that money market funds, generally considered a cash-equivalent, are at all-time highs. This may be linked to pandemic-related jitters for those that sold back during the heightened March market turbulence (at much lower prices). It may also be part of a trend in which overall cash positions tend to rise in election years.

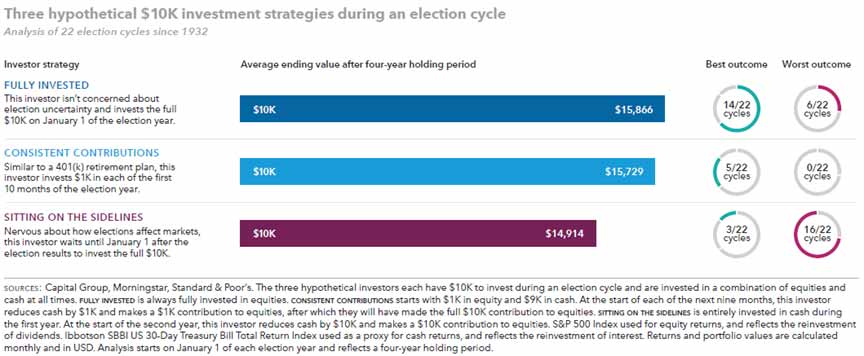

The irony is that short-term timing of total market exposure can cause long-term pain for portfolio returns. A study by Capital Group shows that sitting on the sidelines with cash during election years presented the worst investment outcome in 16 of the past 22 election cycles.

With money market funds and cash essentially paying nothing in today’s zero-interest-rate policy environment, it seems like the safe bet is to stay the course with the long-term investment plan. Additionally, the elevated cash supply tends to be rapidly put to work in the year following an election, which promotes demand for stock exposure and an upward trajectory for stock prices.

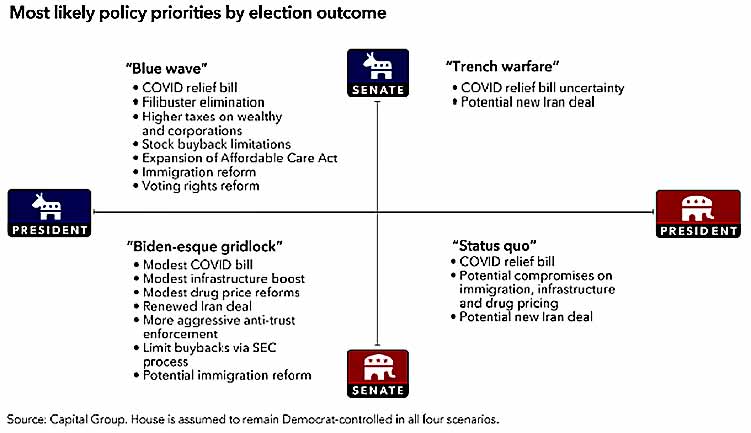

What Are the Possible Outcomes of the 2020 Election?

A significant factor in determining in the pace and breadth of policy change is the amount of gridlock in Washington, D.C.

The House of Representatives, where all seats are up for grabs, is likely to remain with the Democrats. As of October 2, PredictIt had the probability of this at 85%.

The Senate race is where there is more uncertainty, as 35 of the 100 seats are being contested. Of the seats being defended, 23 are currently held by Republicans and 12 by Democrats. It appears close enough that there is potential for the next Vice President to be called upon to cast a vote to decide whether the Senate has Democrat or Republican leadership.

- If the Senate and President stay Republican, a “Red Wave,” we can expect a continuance of the status quo with light corporate regulation, unpredictable bi-lateral trade talks, and a continuance of the Trump tax cuts.

- If the Senate and President are split, then we can anticipate more policy by Executive Order and plenty of contentious gridlock..

- If the Senate and President are Democrat-led, a “Blue Wave,” then we would likely see a combination of tax increases for corporations and higher-income earners, increased regulatory pressures on monopolies that are possibly offset by fiscal spending increases.

While the differences between candidates are stark in many areas, there is more overlap than one might think. No matter the outcome, both parties have expressed their willingness to embrace deficit spending to exit to pandemic-induced economic reality. Further fiscal spending, specifically on infrastructure-related upgrades, seem to be likely bets.

What Are the Market-Based Election Issues?

Tax Policy

A Trump re-election would likely keep tax policy as status quo. For comparison purposes, we will review proposed changes as they are understood today, while aware that details on all of these ideas are sparse, and there is almost no chance they would be enacted as one large package.

Corporate Income Taxes

According to the Tax Foundation, the Biden-led proposal would increase the corporate tax rate to 28% from the current 21%, but still below the 2016 level of 35%

This most impacts low-margin businesses and sectors by reducing post-tax profits.

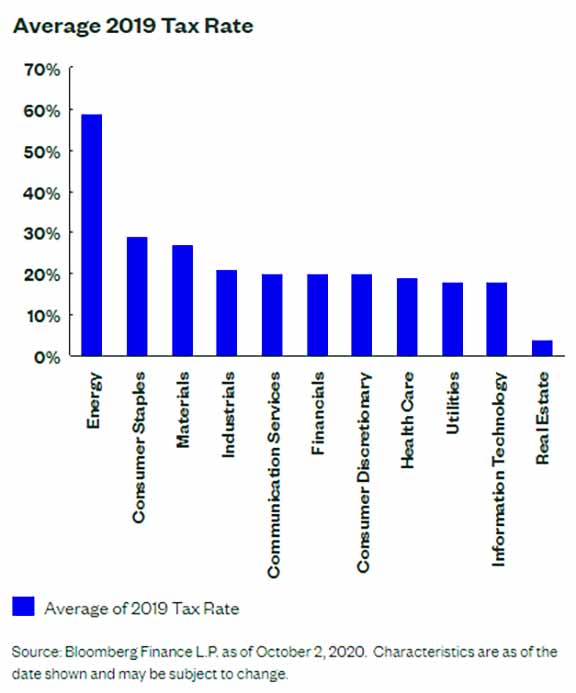

According to data from the NYU Stern School of Business (as of January 2020), among US sectors with the lowest pre-tax unadjusted operating margins were: grocery & food retail (2.3%), food wholesalers (2.7%), autos (3.4%), engineering & construction (3.9%), farming & agriculture (4.0%), general retail (4.2%) and healthcare support services (4.4%).

By comparison, the full market average across 5,878 companies (without financials) was 11.2% with notable high margin sectors being: tobacco (39.3%), railroads (38.7%), water utilities (30.3%), real estate (29.9%), information services (28.3%), REITS (27.2%) and pharmaceuticals (24.9%).

Individual Federal Income Taxes

One of the key features of Joe Biden’s proposed plan is for ordinary income brackets to be adjusted for individuals with annual incomes over $400,000 (although whether this threshold applies to individuals or joint filers remains unclear), increasing the top tax bracket to the pre-Tax Cuts & Jobs Act (TCJA) rate of 39.6%.

The income brackets for those with annual income levels under $400,000 will remain unaffected.

Another feature of Biden’s tax plan is a flat retirement contribution credit, as determined by a specific percentage (currently anticipated to be 26%) of the contribution amount, to replace deductions of those retirement account contributions. This would, in effect, lower the tax burden for taxpayers in tax brackets under the proposed set rate (incentivizing taxpayers in lower tax brackets to contribute to tax-deferred retirement accounts), while increasing it for taxpayers in brackets over the proposed rate.

Few, if any, major tax policy reforms are likely to be enacted until well into 2021. Regardless the makeup of Washington D.C., addressing the pandemic and immediate economic distress will be job number one.

Capital Gains Taxes

Under the proposed tax plan from Joe Biden, the top tax rate for capital gains would jump from 23.8% to 39.6%; however, the rate change only impacts those with more than $1,000,000 in annual income. Given that the top 1% of earners in America are making $500,000 per year, this means that the number of households affected would be rather minimal.

According to Federal Reserve data as of April 2020, the US household share of US equity ownership is roughly 37%. This means that more than 60% of the stock market is owned by institutions, including pension funds, retirement accounts, and foreign investors that are not subject to a capital gains tax.

Financial Transaction Tax

A Financial Transaction Tax has been proposed, which would place a tax ranging from 0.05% – 0.20% on all equity, debt, and derivatives trades transacted in the United States. There is concern that this type of legislature would reduce liquidity in the markets by dis-incentivizing automated and high-frequency trading. As broker commissions have essentially gone to zero, there has certainly been an increase in market liquidity and total participation by retail investors. It can be argued that this has helped keep pricing orderly, even during the most volatile of trading periods. Enactment of this type of tax could reduce liquidity, but it is unclear to what level. Other countries with similar Financial Transaction Taxes include the United Kingdom, France, Switzerland, Taiwan and Hong Kong.

Foreign Policy & Trade

Both leaders are expected to continue tough negotiations with China. Per WisdomTree, though, a more predictable trade negotiation path could be positive for Asian emerging markets and China relations. This would likely promote a more global approach to investing.

A continuation of Trump foreign policy approach would bring more tariff surprises, along with the volatility that comes with those announcements.

There appears to be a bipartisan trend toward onshoring certain manufacturing jobs.

Clean Energy & Infrastructure

Infrastructure spending could have bipartisan support no matter the outcome of the presidential election. A more “green” focus could emerge if a “Blue Wave” wins out. Otherwise, expect a more traditional uptick in the demand for raw materials to build the roads, bridges, and airports.

Regardless of the election outcome, as we have seen, commodities and energy-related companies are highly subject to global supply and demand.

Health Care

Both domestic and global demographics data show that health care needs will remain in high demand for some time. In addition, it appears that continued pandemic-related response provides immediate support to increased production of medical equipment and testing.

Industry disruption with tele-health, genomics, and other biotech innovations will present tremendous opportunities for investment growth moving forward.

Pent-up demand for non-essential medical surgeries will likely assist medical device company revenues over the upcoming years.

Politically, the post-election form of the Affordable Care Act will be up for debate. This adds uncertainty to health care services and insurance providers.

Both parties have committed to lowering prescription drug pricing from pharmaceuticals; however, this sentiment has been swirling for some time with little action to show for it.

Anti-Trust Regulation & Technology

Under a Biden administration, there could be more room for smaller tech-related firms to prosper as larger mega-cap firms deal with antitrust lawsuits and regulation.

Without regulation as a hurdle, we would expect technology firms to continue thriving. Based on Bloomberg Finance revenue data from year-end 2016 to October 2, under the Trump administration, large-cap technology firms had the best sector performance and profit growth, rallying by 156% and seeing annual sales climb from $221 billion to $330 billion.

If the White House and Senate are in political gridlock, it is anticipated that this will be positive for current US technology leaders.

Federal Minimum Wage Increase

A federal minimum wage increase, from $7.25 to $15.00 per hour, would most impact sectors that employ significant amounts of low wage workers, such as hospitality (93.5%), retail (77.4%), arts and entertainment (74.3%), agriculture (72.9%), and logistics (69.0%).

Many states and counties already have higher minimum wage requirements, so the national effect would be less dramatic.

It is also more likely that any changes would be made in stages, rather than immediately.

The Most Dominant Theme

While the November election has grabbed citizens’ attention, we don’t expect the results to be the primary driver of financial markets. As we have reviewed, history shows that the stock market is ultimately indifferent to political parties and rewards those that remain focused on long-term investing.

Typically, a lot of what candidates say during a campaign never comes to fruition, even when a party sweeps an election. The most significant benefit of this type of exercise is to understand the key topics at hand prior to any major action taking place. This is why we don’t alter our investment strategy based on which way the political winds are blowing. Nevertheless, by dialing in on the potential growth catalysts and risks at the macroeconomic, sector, and company levels, we can best be prepared to focus our attention on the real issues that do impact your investment portfolio. This is what helps us sort “the news” from “the noise.”

Currently, the most dominant theme determining the direction of the stock market is a continuation of the economic recovery. We are in an early-cycle economic environment, and policymakers from both sides seem incentivized to support the recovery. This is likely to remain true no matter the election outcomes.

The simple truth is that economic fundamentals, such as corporate earnings, small business growth, investment, the consumer, and innovation, remain more important than political figures and policies. Politicians come and go, but the desire to grow, innovate, and pursue profitable ventures remain a constant.

Our investment approach is not to try and time the absolute top or bottoms of holdings, nor to make high-conviction bets that rely on one particular outcome to perform well. Rather, as stewards of hard-earned capital, we aim to build well-diversified portfolios that are positioned to cautiously capitalize on growth and income opportunities.

We remain committed to a disciplined investment process that helps keeps us proactively aware of the everchanging investment landscape and key market-moving topics.

Regardless of which party controls the White House or Congress, the main driver of investors’ returns over time will be their own asset allocation decisions. It is our role to assist our clients in understanding how their asset allocation is aligned with their investment objectives and lifetime income needs.

What Can You Do Today?

Political winds can shift frequently over time, whereas saving and investing for your financial future is a process that takes place over decades.

I have found that individuals often find the noise of “the news” utterly overwhelming, and I don’t blame them. The information presented over the airwaves often comes in shouts and skews to the negative. Frankly, this is what gets ratings and attention. Unfortunately, it also unfairly biases hard-working people to delay making prudent actions today that improve their long-term financial future.

As an investment professional, I have made it my full-time job to help individuals and families see through the near-term haziness and focus on the big picture of their own financial lives.

The truth is that the best time to take inventory of your personal financial circumstances is now. Your financial success will ultimately be because of the actions you take today, based on factors that are in your control.

Such factors include:

- How much you spend

- The timing of when you spend

- How much you save

- The amount of risk you are willing to take in return for investment return

By speaking with a financial professional that has helped numerous households navigate these complex topics, you can gain clarity on your own financial aspirations, as well as construct a formal plan for real progress toward those desired outcomes.

Disclosure: Derek Pantele is an Investment Advisor Representative with Dynamic Wealth Advisors. All investment advisory services are offered through Dynamic Wealth Advisors. All investments carry certain risks and there is no assurance that an investment will provide positive performance over any period of time. Past performance is not a guarantee or a reliable indicator of future results. The views expressed within are subject to change at any time without notice and are not intended to provide specific advice or recommendations for any individual or on any specific security or strategy..

Are you overpaying taxes?

Take the 2-minute quiz to find out.

EXPLORE TOPICS

Start Your Next Chapter and Pursue Exciting Financial Goals

Click below and schedule a complimentary consultation

Similar Posts

No results found.